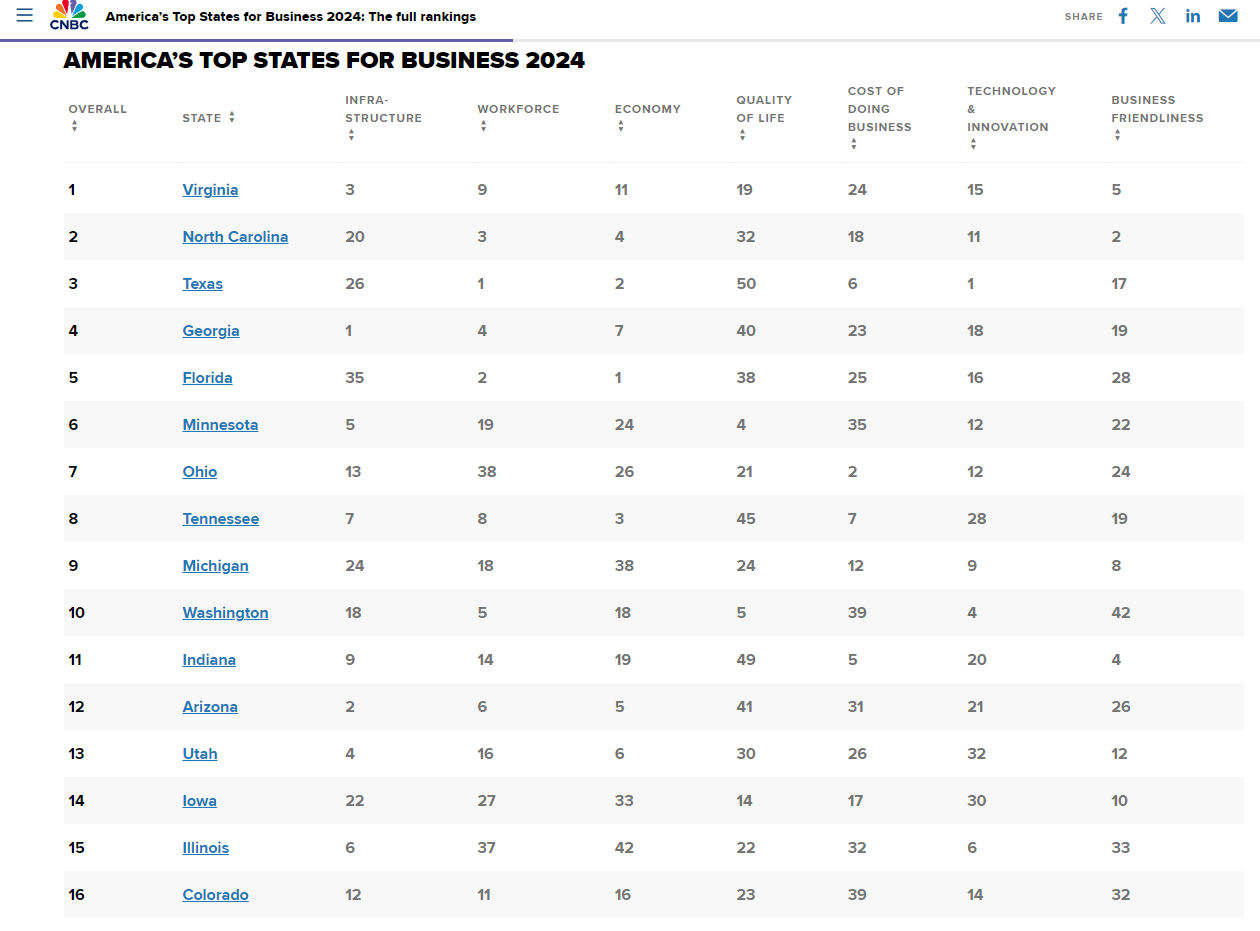

Governor Youngkin addressed a joint meeting of the “money committees” on August 14, reporting continued strength in state revenues and highlighting investments in education, behavioral health, business site development, and natural resources. He signaled continued interest in tax relief, lauding Virginia’s recent selection as CNBC’s top state for business, but noting that “we have work to do” to reduce costs of doing business in Virginia and the cost of living. He encouraged legislators to embrace additional tax relief, paired with further investments in shared priorities.

Secretary of Finance Stephen Cummings presented details on the state’s FY 2024 revenue performance and overall finances; as summarized in the title of one of his slides, “The Commonwealth has never been in a stronger position.” Total state General Fund (GF) revenues were $1.5 billion higher in FY 2024 than in FY 2023, representing 5.5 percent growth over the previous year and outperforming the forecast assumed in the FY 2024 (“caboose”) budget passed in May by $1.17 billion. This forecast, which built on the fall 2023 forecasting process, had assumed a mild recession during FY 2024, which did not materialize. Although job growth at the national level has been slowing, the national economy is still adding jobs, rather than experiencing a decline in employment in the fourth quarter of FY 2024, as the Administration had predicted. Virginia job growth also outperformed expectations, with 1.8 percent growth in nonagricultural employment rather than the predicted 0.1 percent increase.

Secretary Cummings highlighted several aspects of the state’s robust economic health, pointing to strong revenue growth since FY 2019 and improvements in Virginia’s labor force participation rate. He noted that Virginia’s job growth now stacks up well against competitor states such as Georgia and South Carolina. The state’s combined reserve funds now stand at $4.7 billion, in excess of the statutory cap of 15 percent of average annual income and sales tax revenues for the preceding three years (budget language temporarily allows the reserve funds to exceed the cap), and Virginia is ranked third among states with AAA bond ratings for the size of its reserve funds as a percentage of GF expenditures.

As explained in Secretary Cummings’s presentation, the excess FY 2024 revenues are largely dedicated to specific purposes, based on statutory requirements or contingent spending directives included in the budgets adopted in May, such as obligations for I-81 improvements and the Water Quality Improvement Fund, a required set-aside for a deposit to the Revenue Reserve Fund, and funding to address growth in the Virginia Military Survivors and Dependents Education Program. A key task facing the Administration in developing the Governor’s December budget will be determining how much of the revenue growth is likely to be ongoing, which will be part of the forecasting process conducted in consultation with the Joint Advisory Board of Economists (which will meet in October) and the Governor’s Advisory Council on Revenue Estimates (GACRE, which met earlier this summer and will meet again in November). Secretary Cummings explained that although GACRE members generally expected continued economic growth, albeit at a slower pace, when the Council met in July, there are several key points of uncertainty, notably the fate of the Tax Cuts and Jobs Act, which was a signature initiative of former President Trump; provisions of this legislation are scheduled to expire after December 31, 2025, if no action is taken by Congress to extend them. Several of these provisions have direct or indirect effects on Virginia’s tax structure.

Governor Youngkin will present his proposed amendments to the biennium budget on December 18. Secretary Cummings’s slides are available at this link.

Joint Subcommittee on Tax Policy

Following the joint meeting of the money committees, the Joint Subcommittee on Tax Policy held its first meeting of the year. A subset of money committee members serve on this joint subcommittee, which was originally established in 2021 with a broad mandate to evaluate changes to Virginia’s individual income tax system as well as considering other aspects of changes to the state’s tax policies, such as fairness and economic efficiency. The May 2024 budget included a new directive to the joint subcommittee to explore efforts to modernize the state’s income and sales and use tax structure. The August 14 meeting featured a presentation by staff to the Senate Finance and Appropriations Committee on the state’s major revenue sources and a planned schedule for the joint subcommittee’s work; an overview by the Department of Taxation of major state taxes, and a presentation by staff to the Joint Legislative Audit and Review Commission (JLARC) on a 2021-2022 JLARC study on options to make Virginia’s individual income tax more progressive. Although the joint subcommittee is charged with examining state taxes, staff was requested to provide further information to members regarding local collections of real estate taxes, and one member encouraged the joint subcommittee to look at tax reform more broadly, to include local taxes as well as state taxes.

VACo Contact: Katie Boyle